Summary

- The Fed’s Jerome Powell sounded dovish. He noted the rising unemployment rate and inflation getting closer to the Fed’s 2% target.

- Analysts expect the total rate cuts to total 0.50% by the end of 2025.

- The gold price would reach $5,508 per ounce if investors’ responsiveness to rate cuts stays the same.

- The possible downside risks for the stock market and gold include higher tariffs and lower unemployment.

style-photography/iStock via Getty Images

The markets cheered up on Friday as the Fed’s Powell sounded highly dovish about future monetary policies. In my previous article, I wrote about the rather mixed US macroeconomic indicators and the high interest rates that need to be cut in order to prevent the US economy’s health from deteriorating further. Obviously, monetary easing is highly bullish for gold and other precious metals, which I wrote about in many of my previous analyses before. The gold prices also reacted positively to the good news from the Fed. But the question is how much further they can rise and by what time.

My previous article about the Fed

In my previous article about the Fed, I wrote that the US macroeconomic indicators painted rather a mixed picture.

I also wrote about the contracting US economy and tight monetary conditions. I forecast the Fed’s Powell would be dovish during his Jackson Hole speech, thus lifting the financial markets’ valuations even higher. Well, I was right, it seems.

Also, in many of my previous publications about gold, I wrote about monetary easing as a great upside factor for precious metals. According to Powell’s recent speech, there will likely be enough rate cuts in the near future. But what exactly did Powell say?

What did Powell say?

Investors now bet that the Fed will cut rates by 0.25% during its 16-17 September meeting. Some analysts also expect the cuts to total 0.50% by the end of 2025, from the current 4.25%-4.50% level. But why exactly do analysts expect that? Here are the key quotes from Powell’s statement and also my comments. I also marked the most important phrases in bold.

According to Powell,

Inflation had moved much closer to the Fed’s objective, and the labor market had cooled from its formerly overheated state. Upside risks to inflation had diminished. But the unemployment rate had increased by almost a full percentage point, a development that historically has not occurred outside of recessions.

This is a summary of the Fed’s stance change, meaning that inflation has decreased to come close to the Federal Reserve’s 2% target. The labor market, meanwhile, is not as strong as it used to be, even hinting at a possible recession ahead. This is a situation when the Fed traditionally gets dovish.

This year, the economy has faced new challenges. Significantly higher tariffs across our trading partners are remaking the global trading system. Tighter immigration policy has led to an abrupt slowdown in labor force growth… There is significant uncertainty about where all of these polices will eventually settle and what their lasting effects on the economy will be.

This obviously suggests that Powell is worried about uncertainty surrounding the US economy. Economic uncertainty is important for central bankers to become flexible with monetary policies. However, higher tariffs mean higher inflation readings, while a slowdown in labor force growth means lower unemployment. Lower unemployment and higher consumer prices usually make the Fed become more hawkish. But it is unclear if these economic developments will continue in the future because right now the labor market shows signs of a slowdown.

The labor market is a case in point. The July employment report released earlier this month showed that payroll job growth slowed to an average pace of only 35,000 per month over the past three months, down from 168,000 per month during 2024. This slowdown is much larger than assessed just a month ago, as the earlier figures for May and June were revised down substantially…This unusual situation suggests that downside risks to employment are rising. And if those risks materialize, they can do so quickly in the form of sharply higher layoffs and rising unemployment.

So, while the Fed is taking the wait-and-see approach, Powell sees the labor market slowing down.

But the economic growth rate has obviously slowed down, and Powell is admitting this.

At the same time, GDP growth has slowed notably in the first half of this year to a pace of 1.2 percent, roughly half the 2.5 percent pace in 2024. The decline in growth has largely reflected a slowdown in consumer spending.

However, what about inflation? Well, according to Powell, the Federal Reserve is very close to achieving its 2% target.

Measures of longer-term inflation expectations, however, as reflected in market- and survey-based measures, appear to remain well anchored and consistent with our longer-run inflation objective of 2 percent. Of course, we cannot take the stability of inflation expectations for granted. Come what may, we will not allow a one-time increase in the price level to become an ongoing inflation problem.

Despite the Fed’s willingness to react to any changes in inflationary statistics, the current expectations point to the general price level’s stability.

However, here is how Powell summarizes the economic situation:

In the near term, risks to inflation are tilted to the upside, and risks to employment to the downside—a challenging situation. When our goals are in tension like this, our framework calls for us to balance both sides of our dual mandate… Nonetheless, with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.

In other words, despite the tariff risks that could push inflation somewhat up, the unemployment rate’s rise, and the fact the monetary policy is in restrictive territory, there could be more easing ahead.

However, the Fed cannot say for certain where rates will settle out over the longer run, but their neutral level may now be higher than during the 2010s…

In other words, the market should not expect the rates to be close to 0% the way they were after the 2008 crisis or during the pandemic, provided nothing unexpected happens in the near future.

So, what does it mean for the gold prices, and how much higher can the gold prices go, provided we consider only the interest rate cuts?

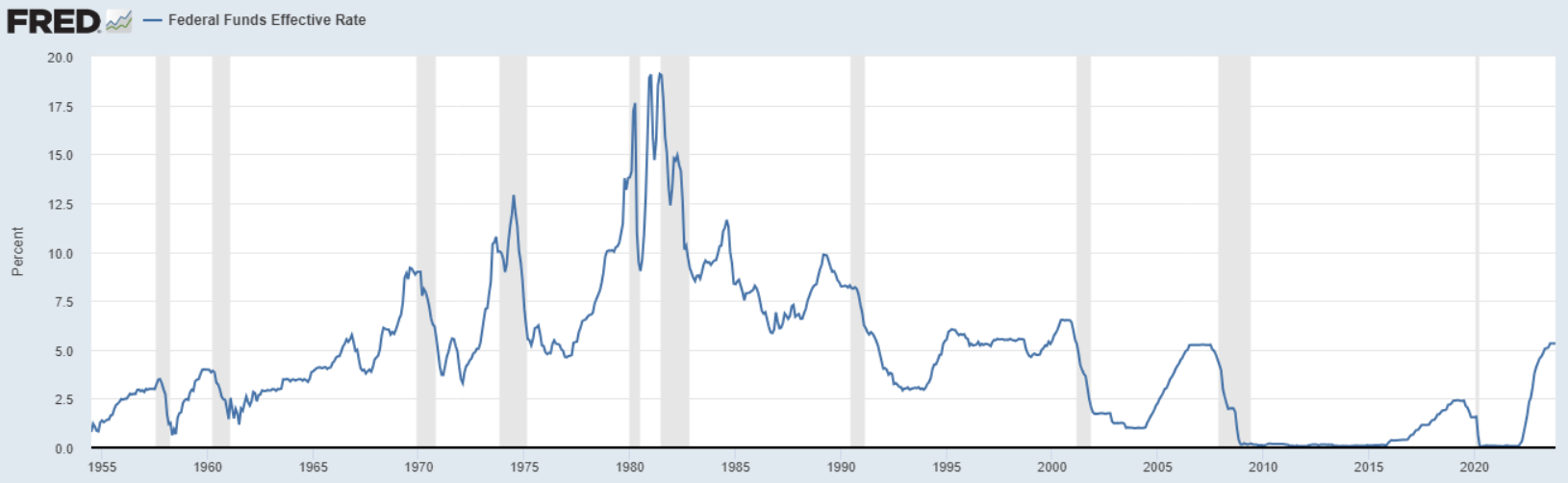

The interest rates, monetary easing and gold price history

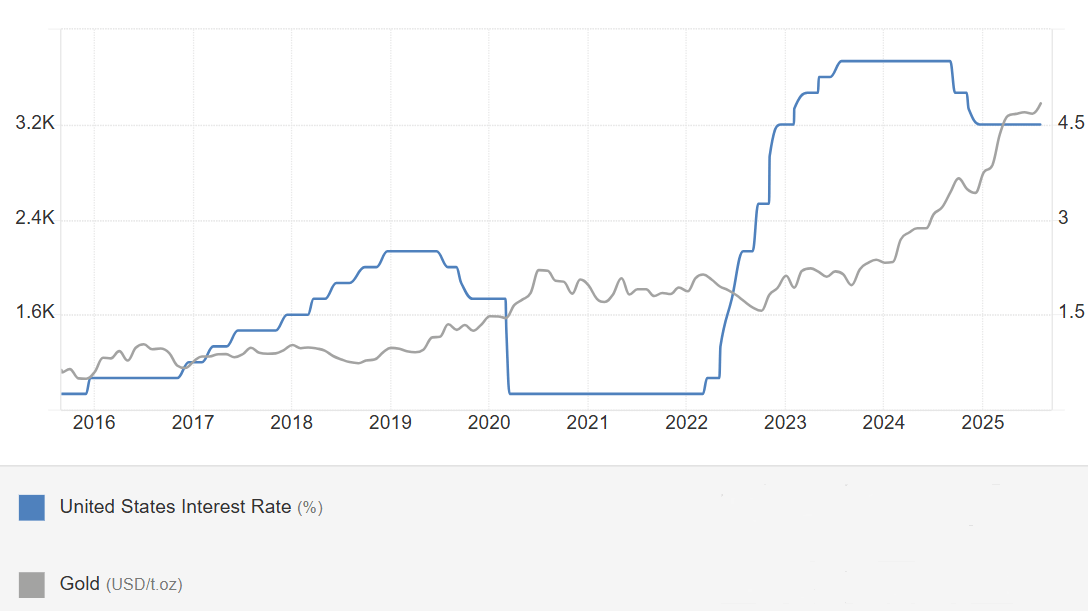

Below I have excerpted a diagram presenting the 10-year histories of interest rates and the gold per ounce prices.

Trading Economics

As can be seen from the diagram above, there is a negative correlation between gold and the interest rates. In other words, when the Fed tightens, gold prices either decrease, remain flat, or stop growing much. However, in 2023, when the interest rates had reached their peak at 5.25%–5.50%, the gold prices started rising rapidly in expectation of more easing ahead. So, in other words, expectations play the key role here.

Since the interest rates’ peak in the 5.25%-5.50% range, they have decreased by 1% to the 4.25%-4.50% range. The rates stayed at this level for most of 2023 and 2024. But how about the gold prices?

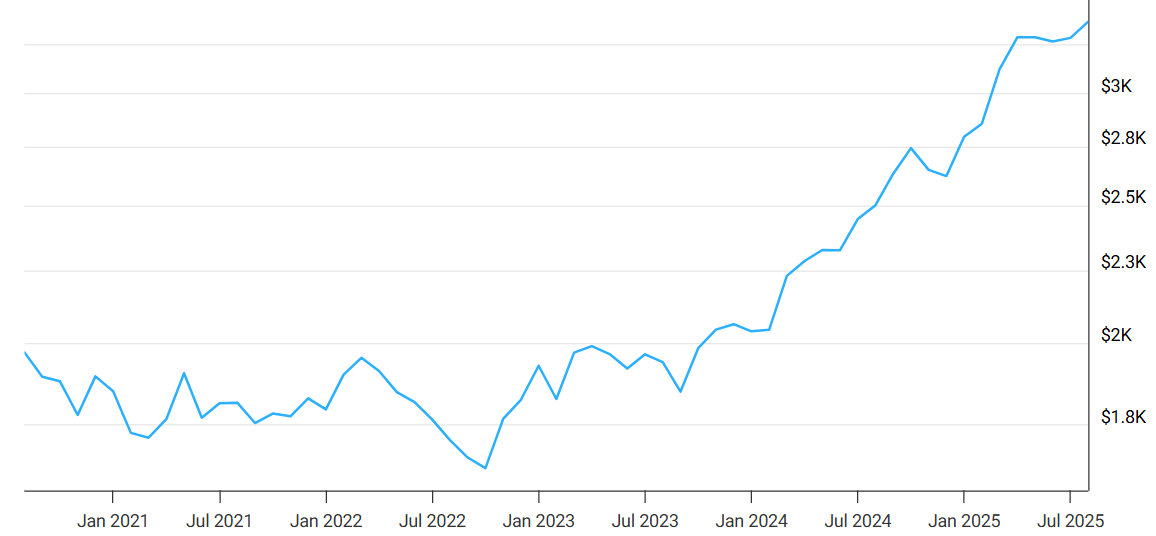

Macrotrends

They used to stay near the $2,000 level during the period. After there was a hint from the Fed that it would start easing its monetary policies, these started rising and reached almost $3,500 per ounce in April 2025. As the gold prices kept increasing, the interest rates were decreasing. So, the $1,500 increase happened over the same time period as the 1% rate decline. For the sake of simplicity, I would like to assume that only the rate cuts made the gold prices rise. Obviously, other factors, including central banks’ purchases and economic and geopolitical uncertainty, also affect the yellow shiny metal’s prices. But I decided to make the ceteris paribus (all other factors being equal) assumption.

$2,000 – 100%

$3,500 – X%

X=175%: There was a 75% gold price increase.

5.25% – 100%

4.25% – X%

X=80.95% – There was almost a 19% interest rate decrease.

So, it seems that gold prices are highly elastic to changing interest rates. If we divide 75% by 19%, we will get a result of 3.95.

So, if we assume the interest rates would decline by 0.50% over the next quarters to total 3.75% and the responsiveness of gold prices to interest rate changes remains the same (3.95, that is), we will see the gold price of $5,508.

4.25% – 100%

3.75% – X%

X=15.94%

15.94% x 3.95 = 62.95%

62.95%+100%=162.95%

162.95% x $3,380 (current gold price) = $5,508

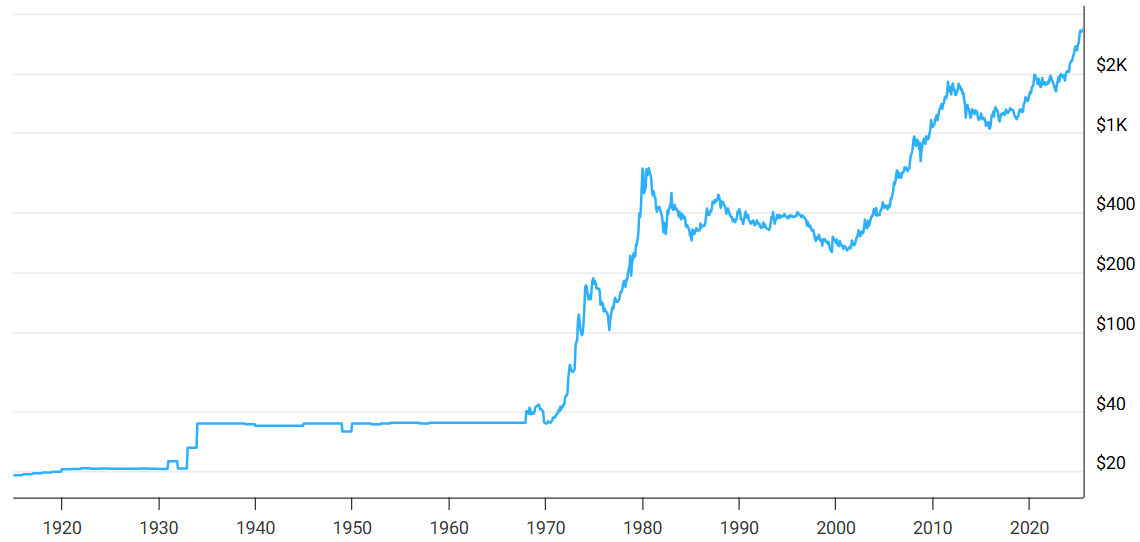

But let me consider two more historical time periods when there was significant gold price growth.

First, it was after the dot-com bubble and lasted until 2011. So, over the time period, the yellow metal’s prices increased more than 6-fold from $264 in 2000 to $1,662 in 2011.

$264 – 100%

$1,662 – X

X=629%

629%-100%=529% growth

So, if we assume gold’s current responsiveness to the Fed’s interest rates and also consider that only the rates mattered for the last couple of years’ rally, gold should trade for $5,508 per ounce after the rate cut by 0.50%.

Macrotrends

Apart from the two recessions during the time period that also boosted the gold prices, there were low interest rates compared to the 1990s. In 1998, these were around 7%, and in 1999, these totaled 7.4%. In the 2000s, meanwhile, the US saw falling rates from a high of around 6.4% in early 2000 to a low of 1.13% by 2003 to battle with the dot-com crisis. But just before the 2008 crisis, the rates were around 5%. After 2008, the interest rates were fixed at 0%. Obviously, the low rates contributed to the extraordinary gold price growth that did not cease over the decade and totaled more than 50% per year if we divide the 529% surge by 10.

The Fed

However, quite an interesting period was during the 1970s when gold appreciated from just $35 per ounce in 1970 to a whopping $618 in 1980, thus totaling an 18-fold rise. That was remarkable because the rates at the time surged from just less than 10% in 1970 to almost 20% in 1980. The price surge in the gold prices, however, was due to very high inflation resulting from uncontrolled money printing by the Fed. As I have mentioned in many of my other articles before, in the 1970s President Nixon abandoned the gold standard—when the USD was fixed to the gold price—to enable more money printing by the Fed to finance the galloping budget deficits. That is why, despite the high rates, investors rushed to buy precious metals. So, these historical periods show that any sort of money supply increase should contribute to a gold price surge.

Risks to my thesis

The downside risks to my thesis include but are not limited to higher than expected inflation making the Fed more hawkish than the market expects. This is a likely result of tariffs. Then, other macroeconomic indicators, including GDP growth, consumer spending, and the employment rate, may improve, thus making the Fed tighten its policies. Obviously, gold would not appreciate as fast as investors would hope to.

However, there are upside factors for gold, including “black swan” events—the Covid-19 pandemic was a good example—and geopolitical uncertainty, including a possible escalation in the Middle East or growing trade tensions. All these factors make the demand for safe havens, most importantly precious metals, surge. In my previous articles, I also mentioned that the US dollar may lose its attraction due to the mounting US national debt and the rise of BRICS+. These factors may even make gold prices exceed my set price target.

Conclusion

The Fed’s Powell sounded dovish while keeping the door open to other economic developments. He admitted the labor market was not overheated, while inflation is moving closer to the Fed’s 2% target. Also, the US economic slowdown has become obvious to the Fed. The situation with lower immigration and higher tariffs, however, may change the macroeconomic indicators, thus making the Fed more hawkish. But there is too much uncertainty here. If the interest rate cuts total 0.50% in the next several quarters, gold’s miraculous rally may continue. The yellow metal may even touch the price of more than $5,500 per ounce, assuming all other factors stay the same.

Anna Sokolidou: I’m a research analyst and a freelance writer looking for value investment opportunities. I have several years of investing experience. I am mostly interested in writing about bargain stocks of large companies. My interest is not limited to American companies but extends to firms operating in other countries but listed on US stock exchanges.

Analyst’s Disclosure:I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Shared by Golden State Mint on GoldenStateMint.com